The Efficient Market Theory states that fluctuations in price of a share are random and do not follow a regular pattern.

Hence, the amount paid for a stock or security and the return when discounted based on the amount of risk it involves will give a Net Present Value equal to Zero (NPV = 0), i.e. there is no way to beat an effective market consistently. This is because all current and relevant information is already reflected in the share price.

Concepts of Efficient Market Theory

• Market Efficiency – An efficient market is a market that provides fair return to its investors. This is possible only when the market is able to quickly and accurately reflect the expectations of investors in share prices, this is known as market efficiency.

It can be of two types: Operational Efficiency and Informational Efficiency.

While Operational efficiency of a market is determined on the basis of time taken to execute an order and number of bad deliveries, Informational Efficiency in a market is determined on the basis of swiftness and accuracy of the market to adjust itself in reaction to new information (economic reports, company analysis, political agendas, government policies etc.).

• Liquidity Traders – Traders who do not buy or sell shares on the basis of research and analysis but on the basis of their individual fortune and liquidity needs are liquidity traders.

• Informational Traders – Traders who buy or sell shares on the basis on thorough research and analysis of the market are informational traders. They usually invest of the basis of differences in intrinsic value and market value of a security.

Assumptions of Efficient Market Theory:

- There are large number of buyers and sellers for a security

- All investors act rationally with the motive of making profit

- New information arises randomly and is available to all market participants for free

- Prices of securities respond quickly to newly available information and reflect all available information

The Random-Walk Theory

This Random Walk theory was propounded by Professor Eugene Fama. It stated that an efficient market fully reflects the available information in share prices. Hence, if the markets are efficient, security prices will reflect normal returns for level of risk associated with the security. Fama suggested three forms of market on the basis of market efficiency and type of information considered in the market.

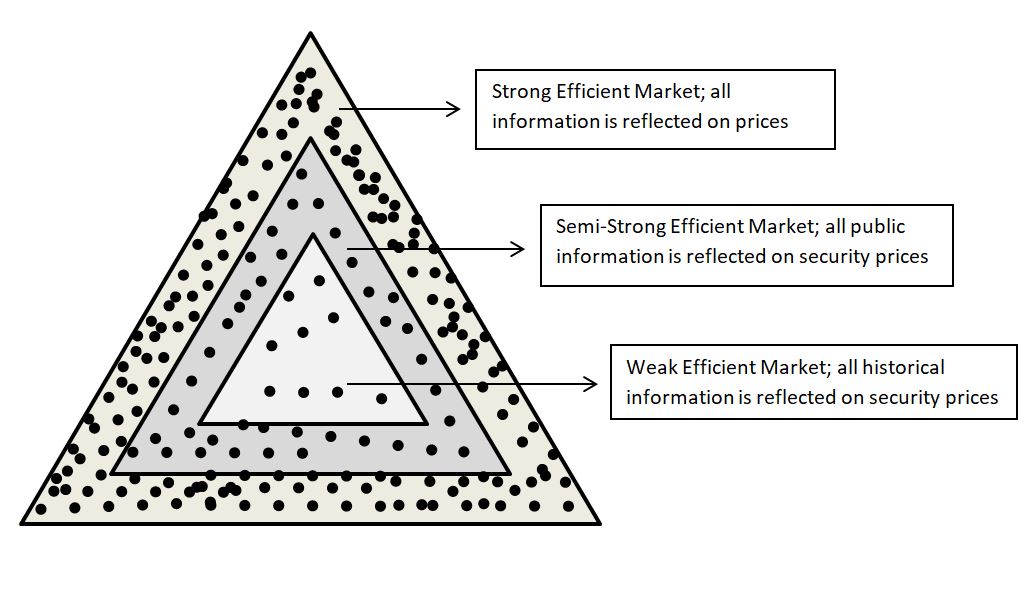

Forms of Efficient Market (Strong, Semi Strong, Weak)

• A Weak Form of EMH makes use of only historical information and states that all historical information found in past prices and volume of trade is reflected in current prices. It suggests that all new public and private information may not be available to all investors, while all historical information is available with all investors; hence all information is not translated in current prices. Therefore future prices cannot be predicted by analysing historical prices. In such a market, liquidity traders cause price fluctuations as they sell their shares without considering its intrinsic values; while the buying and selling activities of informational traders result in alignment of market prices with intrinsic values.

• A Semi-Strong Form of EMH makes use of historical data as well as publically available information and states that all historical and public information is available with all investors and is translated into current prices. Hence whenever new information arrives in the market, it is quickly reflected in security prices. In such a market informational traders can earn huge profits in a short run while liquidity traders with naïve buy and hold policy will incur losses.

• A Strong From of EMH takes into account all public, private and historical information and states that all information is fully reflected in current prices even though private information may not be available with all investors, but only with few insiders(CEO`s of the company, Board of directors etc.).

Hence all information historical, public or private is useless in predicting the future values and there is no way to consistently beat the market.