The Reserve Bank of India – RBI is the Central Bank of the country. It has the task of overseeing the economic as well as the monetary policy of the country.

History of RBI

The Royal Commission on Indian Currency and Finance, which was also known as the Hilton-Young Commission, recommended the creation of a Central Bank. The recommendation was based on the principle of separation of control of currency and credit from the other functions of the Government and to facilitate the growth of the banking sector. The Reserve Bank of India Act, 1934 paved way for the creation of the Reserve Bank and operations started from the year 1935. Since, then the Reserve Bank of India has undergone numerous transformations, reflecting the growing aspirations of the country.

Functions of RBI – Reserve Bank of India

The functions of the Reserve Bank of India is broken up into three heads:

- Traditional Functions

- Development Functions

- Supervisory Functions

Tradition Functions

- Primary Banker to the other banks within the country

- Banker to the Central and State Governments

- Management of foreign exchange reserves

- Foreign exchange management—current and capital account management

- Overlooking the Monetary policy of the country

- Regulation of money, forex and government securities markets as also certain financial derivatives

- Debt and cash management for Central and State Governments

- Oversight of the payment and settlement systems

Development Functions

- Promoter and the key driver for Developmental role

- Agricultural development

- Industrial Finance

- Promotion of Export

- Research and statistics and Technical advisory to the government

Supervisory Functions

- In charge of the Currency management mechanism

- Regulation and supervision of the banking and non-banking financial institutions, including credit information companies

- License provider to banks

- Supervision of Banking performance

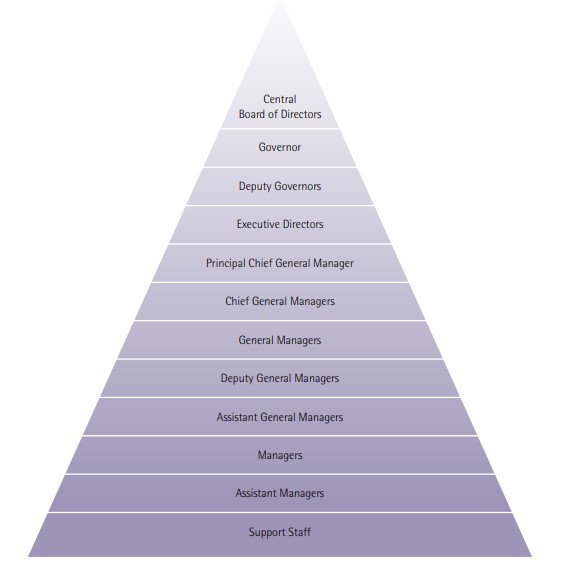

Management Structure of RBI – Reserve Bank of India

Central Board of Directors

They are the top bosses of the organization and hence are located at the top of the heap. The post was created through the Reserve Bank of India Act, 1934, and has the responsibility to oversee the functioning of the central bank. It is also in charge of delegating roles and responsibilities to the others ie. Local boards and the other committees.

Governor, Deputy Governor, and Executive Directors

The Governor is the Chief Executive of the Reserve Bank. His/her role is to supervise the working of the bank and be a part of its daily operations. His management team consists of the Deputy Governors and Executive Directors.

The Central Government has the responsibility of nominating fourteen Directors on the Central Board. This includes at least one director from each of the local boards.

The remaining ten directors represent the different sectors of the country, namely, Trade, industry, agriculture, etc. The appointees are scheduled to chair their positions for a maximum period of four years.

The Central Government also nominates a Government official in the post of a Director. This official will be representing the government. The Finance secretary is usually selected as the member of the board and its term is fixed as per the requirement of the Central Government. The Governor, as well as a maximum of four other members, are the ex officio Directors of the Central Board.

The Local Boards

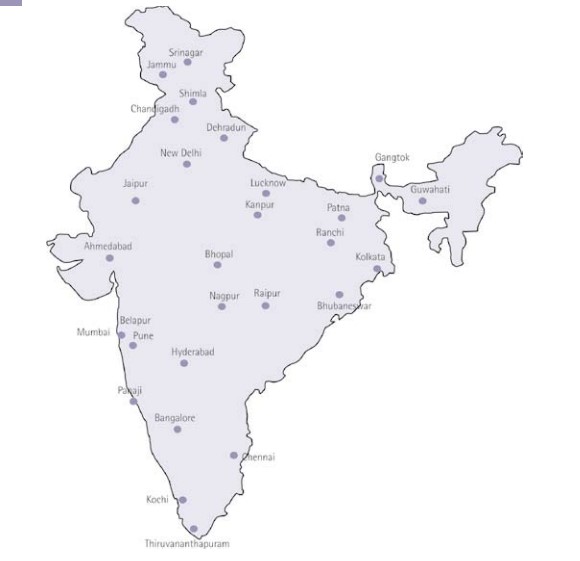

The Central Government has constituted four local boards each representing the four major areas of the country: North, South, East, and West.

The respective headquarters are:

- North: New Delhi

- South: Chennai

- East: Kolkata

- West: Mumbai

Each of these local boards has 5 members each, nominated by the Central Board, having a term of 4 years. These individual boards represent the territorial area they have been assigned to and advise the Central Board on issues related to the local economy and financial structures. The Central Board delegates other functions to the Local Boards too.

Offices and Branches

The RBI has offices and branches spread across the length and breadth of the country. The 4 main offices are the ones operating from the four main metros: New Delhi, Chennai, Kolkata, and Mumbai. There are 27 other offices and branches. The larger offices and the branches are headed by a senior officer designated as the Chief General Manager. They also act as the Regional Director. The smaller branches are headed by a senior officer designated as the General Manager.

The Reserve Bank of India has over the years kept transforming itself as per the demands of a growing economy. It has added departments, merged few, even closed a few down. The below list is of the departments which are in existence now:

Central Office Departments

- Department of External Investments and Operations

- Financial Markets Department

- Financial Stability Unit Internal Debt Management Department

- Monetary Policy Department

Regulation and Supervision

- Department of Banking Operations and Development

- Department of Banking Supervision

- Department of Non-Banking Supervision

- Foreign Exchange Department

- Rural Planning and Credit Department

- Urban Banks Department

Research

- Department of Economic Analysis and Policy

- Department of Statistics and Information Management

Services

- Customer Service Department

- Department of Currency Management

- Department of Government and Bank Accounts

- Department of Payment and Settlement Systems

Support

- Department of Administration and Personnel Management

- Department of Communication

- Department of Expenditure and Budgetary Control

- Department of Information Technology

- Human Resources Development Department

- Inspection Department

- Legal Department

- Premises Department

- Rajbhasha Department

- Secretary’s Department

Other than these departments, the Central Board also has the task of overseeing various other financial activities through its myriad boards and committees.

Board for Financial Supervision (BFS)

This Board formed through Section 58 of the RBI ACT and came into being in the year 1994. It was formed to be a committee of the Central Board whose primary focus was to undertake supervision of all the different sectors of the financial system, in an integrated manner. The entities which are part of this sector are:

The Chairman of the BFS is the Governor himself/herself, while the Deputy Governors are the ex-officio members. The Vice-Chairperson is usually a nominated post and is held by the Deputy Governor in-charge of banking regulation and supervision. Four Directors from the Central Board are nominated as members of the board. The nomination is done by the Governor himself/herself.

It is mandatory for the board to meet at least once a month and deliberate on issues ranging from regulatory controls to supervisory reports. These supervisory reports are a result of the surveillance carried out by the Supervisory departments of the Reserve Bank of India. These reports help in giving directions for the formulation of policy.

Hence, the board plays a critical part in helping the Reserve Bank of India discharge its role in regulating and formulating monetary policies.

Audit Sub Committee

An audit subcommittee has been created under the BFS to oversee activities that will continuously improve the audit-related exercises undertaken by the Reserve Bank of India. The Audit subcommittee overlooks both internal and external audits. This subcommittee is headed by the Deputy Governor in charge of regulation and supervision. The other members of this unit are two Directors from the Central Board.

Board for Regulation and Supervision of Payment and Settlement Systems (BPSS)

Any policy initiatives on payments and settlements are overseen by this unit. It is headed by the Governor of the Reserve Bank while its members consist of two Deputy Governors, three Directors from the Central Board, and members on invite who are domain experts.

The BPSS has the mandate to lay down policies meant for regulation and supervision of payment and settlement systems, build standards for systems, authorize systems, and lay down rules for their membership.

There are a group of fully-owned subsidiaries under the Reserve Bank of India:

Deposit Insurance and Credit Guarantee Corporation (DICGC)

The DICGC came into being on July 15, 19978 after being established under the DICGC Act 1961. It is responsible for the insurance of all deposits such as savings, fixed, current, and recurring deposits. However, it does not have jurisdiction over the following entities:

- Deposits of foreign Governments;

- Deposits of Central/State Governments;

- Inter-bank deposits;

- Deposits of the State Land Development Banks with the State cooperative

- bank;

- Any amount due on account of any deposit received outside India;

- Any amount, which has been specifically exempted by the

- A corporation with the previous approval of the Reserve Bank of India.

The DICGC insures the deposited amount of up to INR 1,00,000 and pays out that amount in the event of the bank undergoing liquidation.

National Housing Board (NHB)

Set up on July 9, 1988, the NHB is a fully owned subsidiary of the RBI and acts as the apex institution related to housing. The responsibilities of the NHB are:

- To integrate the housing finance system with the overall financial system.

- To promote a financially sound housing financial system

- To create an affordable housing credit system

- To promote affordability by promoting augmentation of supply of land and building material

- To regulate the companies involved in housing finance

Bharatiya Reserve Bank Note Mudran Private Limited (BRBNMPL)

Established in 1995, this wholly-owned subsidiary is responsible for the production of banknotes in India. It has two presses. One at Mysore and the other at Salboni. Its registered office and corporate office are located in Bengaluru.

National Bank for Agriculture and Rural Development (NABARD)

National Bank for Agriculture and Rural Development (NABARD) is an institution whose majority stakeholder is the RBI. It is mandated to facilitate the uninterrupted flow of credit for development and promotion of agriculture, cottage, village, rural crafts, and small scale industries. It also oversees all other economic activities, sustainable rural developments, and promote prosperity in its area of concern.

The RBI strength as of December 31, 2017, is 14,785.

Training and Development

RBI is a knowledge-based organization whose primary focus is to regulate the financial structure and system of the country and promote fair monetary policies. Hence, it has to have a rigorous training and development program.

The RBI has two training colleges and 4 zonal training centers.

The Reserve Bank Staff College, also known as the Staff Training College, was established in the year, 1963 and trains its junior and mid-level officers as well as staff from other banks. It offers courses in Broad Spectrum, Functional, Information Technology, and Human Resources Management and these are all residential programs.

The College of Agricultural Banking was set up in Pune in 1969, trains the senior and the middle-level officers about rural and cooperative credit sectors. It has also currently expanded its training expertise towards subjects as diverse as non-banking financial companies, human resource management, and information technology.

In addition to these centers, the RBI has four Zonal Training Centres located in Chennai, Kolkata, Mumbai, and New Delhi, where it trains its clerical and sub staff. These zonal training centers are also being used to train junior officers.

Other than the training and development centers the RBI has under its wing a few autonomous institutions.

National Institutions

- Institute of Bank Management (NIBM), Pune

- Indira Gandhi Institute for Development Research (IGIDR), Mumbai

- Institute for Development Research in Banking Technology (IDRBT), Hyderabad

The NIBM acts as think tank of the RBI and is engaged in research and education. It plays an important role in training senior bankers and finance administrators. It also provides consultancy to the banking and financial sectors.

The IGIDR is engaged in advanced research on development issues. It offers a Ph. D program in the field of development studies. In 1995, an M.Phil program was also launched. This is an institute that is fully funded by the RBI.

The IDRBT was established in 1996 as an Autonomous Centre for Development and Research in Banking Technology. The primary focus of this institute is to improve banking technology in the country. Currently, it is working on areas like:

- Financial Networks and Applications

- Electronic Payments and Settlement Systems

- Security Technologies for the Financial Sector

- Technology-Based Education

- Training and Development

- Financial Information System

- Business Intelligence

The institutes are actively involved in improving various standards and systems for the banking sector in conjunction with the RBI, Indian Banks Association, Ministry of Communications and IT, GOI, and the various other committees.

Reserve Bank and its relationship with Commercial Banks

The relationship between the RBI and the Commercial Bank needs to be seen from the angle of both legal and regulatory ones. RBI gets its mandate on the basis of the RBI (Reserve Bank of India Act) ACT 1934 while the commercial banks function under the Banking Regulation Act 1949.

The Reserve Bank of India is the head of all monetary policies in India and supervises all the banks irrespective of their affiliations.

The RBI enjoys wide powers. it issues currency notes, provides liquidity to commercial banks, it regulates the money supply and liquidity (through various instruments), audits the books of commercial banks, and can suspend operations of a bank if there are serious financial irregularities to be found. It acts as the lender of the last resort to the commercial banking system.

The RBI also regulates the banking functions. That would mean it has the authority to assess the financial health of the bank through financial surveillance and surveys. This is done to safeguard investments and deposits and also to check that they work on fair principles.

Good blog!

Happy every day!

This is a good blog, happy every day