The Working Capital Requirement of a business is the sum of current assets or the amount of funds necessary to cover the cost of operating expenses of the business.

The two main components of working capital are current assets and current liabilities. The excess of current assets over current liabilities is known as working capital.

Working Capital = Current Assets – Current Liabilities

It is simply the cash required for purchase of raw materials and their conversion into finished products.

Gross Working Capital – It is the capital invested in total current assets.

Net Working Capital – It is the excess of current assets over current liability.

Components of Working Capital

| Current Assets | Current Liabilities |

| Cash in Hand, Cash at Bank | Bills Payable |

| Bills receivable | Sundry Creditors |

| Short term loans | Outstanding Expenses |

| Sundry debtors (less provision for bad debts) | Payment of dividend |

| Prepaid Expenses | Bank overdraft |

| Accrued Income | Taxes |

| Inventories: Raw Materials, Work in Progress, Stores and Spares, Finished Goods |

Types of Working Capital

- Permanent Working Capital – Funds necessary to carry the operations of a business.

- Temporary Working Capital – Seasonal or special requirements for funds.

- Semi-variable Working Capital – The fund requirements remains same up to a stage, then increases with sales and time.

Determinants of Working Capital Requirement

- Nature of Business – In small trading businesses, the initial investment on fixed assets is low and the working capital requirements are high, whereas big Trading houses incur more investment on initial fixed capital than working capital.

- Size of Business – By virtue of its size a large business with wide range of activities require more working capital than a small business.

- Production Cycle – In case of continuous production Working Capital requirements will be high and low in case of intermitted production.

- Business Cycle – WC requirements are high in boom period and less at the time of depression in the economy.

- Production Policy – If the company has the policy to stop/reduce production during slack periods and fluctuations their working capital requirement is low but if it continues production at full scale even in slack season it will incur a high working capital.

- Credit Policy – If the company purchases Raw material on credit basis and sells finished goods on cash basis, it will have low working capital requirements but in the reverse scenario working capital requirements will be high.

- Availability of Raw Materials – If raw material is readily available the company will have a low working capital, but if the raw material is scarce, the company will incur a high working capital.

- Earning Capacity – Firms with high earning capacities are able to earn more cash profits that can be contributed towards working capital requirements, while firms with less earning capacity will have a high working capital.

- Level of Taxes – High level of taxes indicate a high Working capital while low level of taxes indicate a low working capital as taxes cut down profits of companies which in turn focus on higher productivity and high sales of products which require a high working capital.

- Nature of Demand – If the demand for the company`s product is high it will incur a high working capital, but if the demand for the company`s product is low it will incur less working capital.

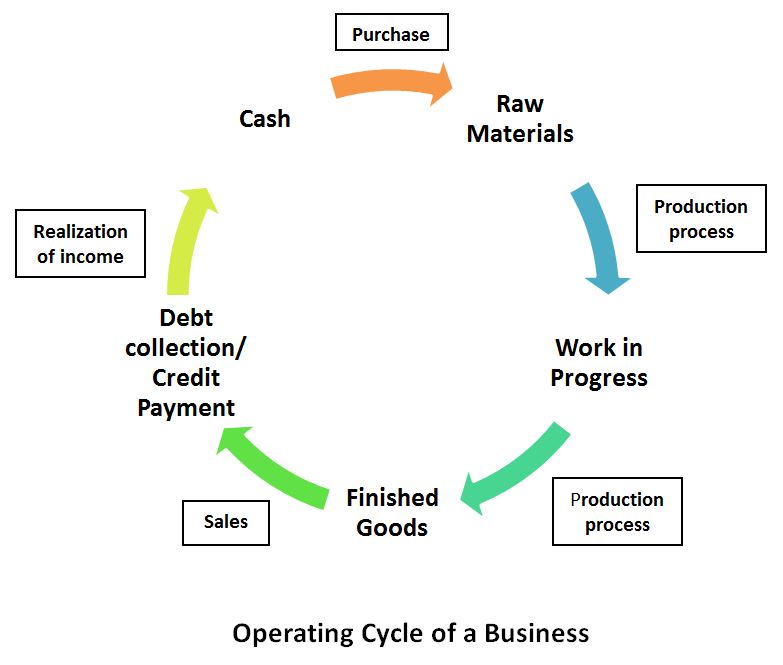

Working Capital Cycle OR Operating cycle OR Cash Conversion Cycle

Working capital requirement depends upon the operating cycle of the business. The operating cycle or working capital cycle of a business starts with the acquisition of raw materials and ends with the collection of receivables from sale proceeds.

The Operating cycle of a business determines its working capital requirement. The Total time period involved in an operating cycle is the sum total of time taken to carry out two important steps i.e.

- Inventory conversion Period – Total time taken in production and sale of products.

- Debtors conversion Period – Total time taken to collect the outstanding amount from customers.

The Operating cycle includes the following stages-

- Raw material and storage stage (R)

- Work in Progress stage (W)

- Finished Goods stage (F)

- Collection of Receivables and Debtors Collection (D)

- Payment to Creditors (C)

Gross Operating Cycle = R + W + F + D

The Net operating cycle represents cash conversion cycle.

Net Operating Cycle = R + W + F + D – C

Increase in operating cycle =

Difference in time taken for debt collection + Difference in time taken in credit payments

Less

Difference in finished goods + Difference in stock of Raw material

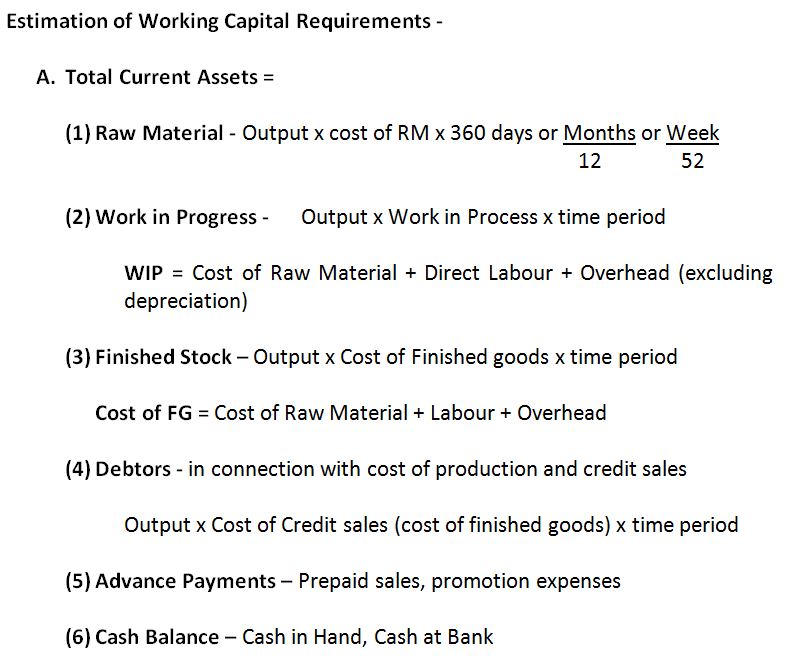

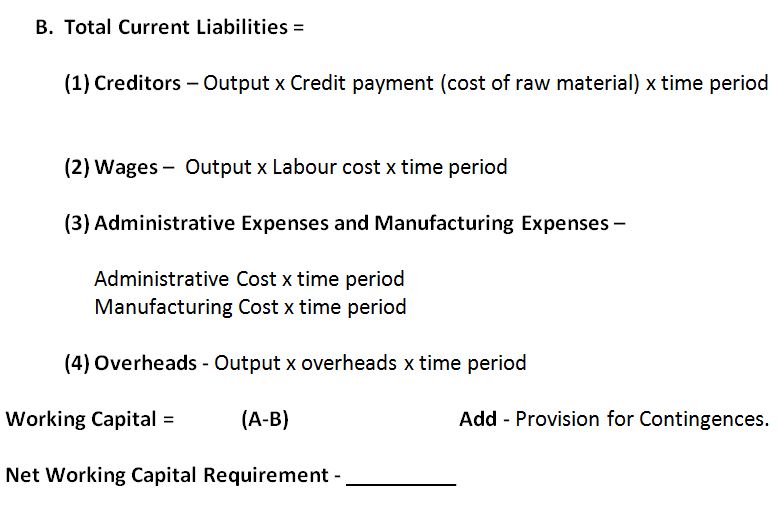

Statement of Working Capital Requirement

need a copy of the artivle in PDF

Thanks

there is no examples of calculation

Hi, We will add an example as soon as possible. Please subscribe and you will receive the update notification.

need a copy of pdf the above notes