Investment refers to employment of funds on assets with the aim of earning income or capital appreciation.It is essentially a sacrifice of current money or other resources for future benefits.There are various Investment Alternatives available with an investor. An investor has to carefully choose between different investment alternatives like negotiable securities (Can be freely traded in the market) and non-negotiable securities(cannot be traded in the market), Mutual Funds and Non-Financial Instruments or Real Assets. Negotiable securities can be fixed income (bring fixed returns) or variable income securities (brings variable returns).

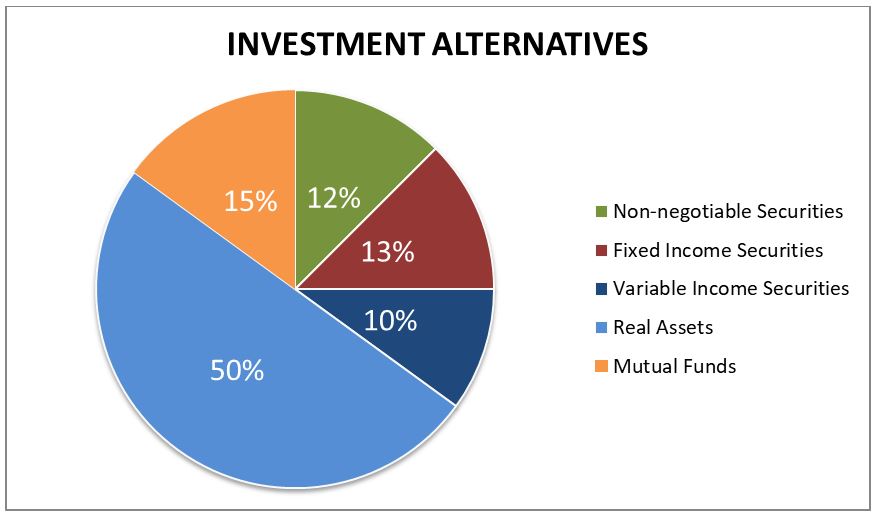

The chart below attempts to show a basic investment strategy of an investor. Percentage of total income to be spent on various investment alternatives are:

Different Investment Alternatives

(1) Negotiable Instruments / Securities –

These investment alternatives can be traded in the market.

(i) Variable Income Securities

• Equity Shares: Shares which do not carry any preferential rights in repayment of capital and dividend payments are equity shares. The rate of dividend is not fixed and varies depending upon the profitability, financial position and business objectives of a company. The owners of equity shares are the owners of the company and have voting rights in the management of the company.

Classification on the basis of nature of shares:

- Growth Shares: These stocks have a higher growth rate than the industry growth rate on the basis of profitability. E.g. HCL

- Income Shares: These stocks have a relatively stable operations and limited growth opportunities. E.g. Banks, FMGC, Cadbury, nestle, Hindustan lever

- Defensive Shares: These shares are normally not affected by the movements in the market. E.g. Pharma Stocks

- Cyclical Shares: These stocks are affected by the business cycles. The upward and downward movements of business cycles affect the profitability of the company and also the share price of a company. E.g. Automobile stocks

- Speculative Shares: These shares have a lot of speculative trading. They attract the investors in bull and bear phases of the market.

(ii) Fixed Income Securities

• Preference Shares – Shares which carry preferential rights in respect of dividend payment and repayment of capital are preference shares. These shares carry a fixed rate of divided and preference over equity shareholders in dividend payment and payment of capital at the time of liquidation. They do not carry any voting rights.

• Debentures – These are capital market instruments used to raise medium and long term capital funds from the public. It comprises of Periodic interest payments over the life of the instrument and principle payment at time of its redemption. These are for investors who wish to sacrifice liquidity for high returns.

• Bonds – They are similar to debentures but are issued by public sector companies. Its value in the market depends upon the interest rate and maturity of the bond. The coupon rate is the nominal interest rate offered on the bond which cannot be changed till its maturity. E.g. Education benefit bond, retirement benefit bond.

• IVP`s and KVP`s – These are savings certificates issues by the post office with the name Indra Vikas Patra and Kisan Vikas Patra. IVPs have a face value of 500,1000, 5000 and KVPs have a face value of 1000, 5000, 10000. The capital is doubled in 5.5 years with 13.47% rate of return. They do not carry any tax benefits but are transferable just like bearer bonds.

• Government Securities – These are secured securities issues by the central and state government. The rate of interest on these securities is relatively low but they are highly liquid and safe.

• Money Market Securities – These securities have very short term maturity usually less than a year. E.g. Treasury bills, Commercial paper, Certificate of Deposit

(2) Non Negotiable Instruments / Securities – These investment alternatives cannot be traded in the market.

• Deposits: Deposits earn a fixed rate of return.

- Bank Deposits – Banks usually offer three traditional facilities, they are; current account facility (no interest is paid), savings account (4-5% interest is paid) and fixed account (7-8% interest is paid).

- Post Office Deposits – Fixed deposit and Income schemes at Post offices provide around 13% to 15% interest rate.

- NBFC Deposits – NBFC`s having bet owned funds over 25 lakh can accept deposits with maturity ranging from 3-5 years and provide interest rate higher than commercial banks.

• Tax Sheltered Savings Scheme – These are beneficial for tax-paying Investors. They offer tax relief to its participants according to the taxation laws. E.g. Public Provident Fund Scheme, National savings scheme, National Saving Certificate, Public Provident Fund Scheme, National Savings Scheme, National Savings Certificate

• Life Insurance – It is a contract for payment of a sum of money to the person assured or entitled on happening of an insured event or at maturity. It also provides tax benefits to the person buying the insurance scheme. E.g. Basic Life Insurance: Whole Life Assurance Plan, Endowment Assurance Plan, Term Assurance Plans, Plans for Children, Pension Plans

(3) Mutual Funds

A mutual fund is a professionally-managed investment scheme, usually run by an asset management company that brings together a group of people and invests their money in stocks, bonds and other securities.

An investor can buy mutual fund ‘units’ which represent his/her share in a particular scheme. These units can be purchased or redeemed as needed at the fund’s current net asset value (NAV). These NAVs keep fluctuating, according to the fund’s holdings. All the mutual funds are registered with SEBI.

• Open Ended Mutual Fund Schemes – These offer its units on continuous basis and accept funds from investors continuously. There are no restrictions on buying or selling funds. These schemes do not have a maturity period and are not listed on the stock exchange. These provide liquidity to investors since repurchase facility is available.

• Closed Ended Mutual Fund Schemes – These have a fixed maturity period and are kept open for a limited period. Once closed the units are listed on the stock exchange. The demand and supply factors influence the price of the units.

Types of Mutual Fund Schemes

- Growth Schemes – These funds invest money in equities and offer high returns.

- Income Schemes – These funds invest money in fixed securities and provide a regular return to its holders.

- Balanced Schemes – These funds provide a steady return as well as a reasonable growth. The money is generally invested in equity and debt instruments.

- Money Market Schemes – These funds invest money in money market instruments like TB, CP.

- Tax Savings Schemes – These offer tax rebate to its investors. Equity linked saving schemes and pension schemes provide exemption from capital gains on specific investment.

- Index Schemes – These funds invest on equities of the index. The returns are approx. equal to the return of the Index.

(4) Non-Financial Instruments or Real Assets

These Investment alternatives usually form the major part of the investor`s portfolio. They include:

- Gold and Silver – They provide best protection against inflationary tendencies in an economy.

- Real Estate – They provide high returns to investors but require high investment and long term commitment. This investment alternative includes investment on land, buildings, any personal and property.

- Antiques – They usually guarantee safety of investment. A price rise is generally due to increased interest of collectors or increased social importance.

Thanks very interesting blog!