Performance Budgeting refers to a budget in terms of functions, programmes and performance units (functions, activities and projects) reflecting the revenues and expenditures of an Organization or Government. Performance Budgeting refers to a budget in terms of functions, programmes and performance units (functions, activities and projects) reflecting the revenues and expenditures of an Organization or Government.

Features of Performance Budgeting

♦ Performance Budgeting provides

- The purpose and objectives for which funds are required

- Costs of programs and related activities proposed to accomplish those objectives

- The output that will be produced under each activity.

♦ Performance Budgeting implies that the budget must clearly indicate the actual achievement or output, expected by spending a particular amount on a particular activity. Hence, It is an output oriented budget that focuses more on achievement rather than means of achievements.

♦ The costs and benefits of each activity are analysed for making decisions regarding allocation of funds.

♦ It involves use of management tools such as – work measurement, bench marking and unit costing etc. to prepare a budget.

♦ This system has been designed to plan for long term.

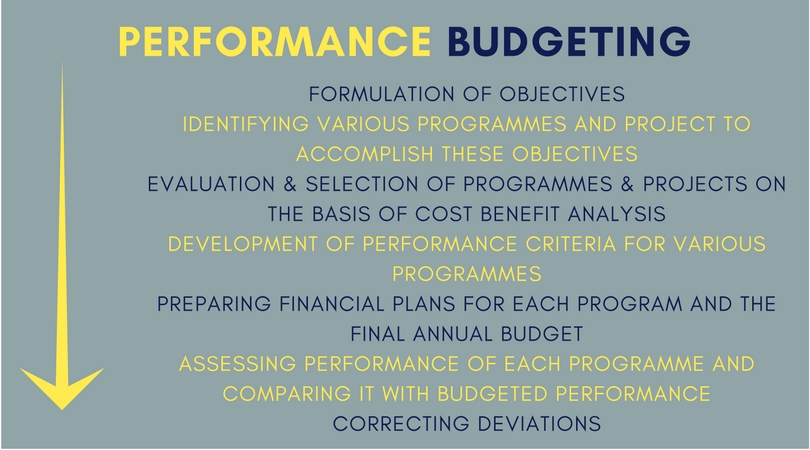

Process of Performance Budgeting

- Formulation of objectives

- Identifying various programmes and project which will accomplish these objectives

- Evaluation & selection of programmes & projects on the basis of cost benefit analysis

- Development of performance criteria for various programmes

- Preparing financial plans for each program and the final annual budget

- Assessing the performance of each programme an comparing the same with budgeted performance

- Correcting deviations

Advantages of Performance Budgeting

- It states clearly the purpose & objectives for which funds are needed.

- It improves performance of units in a continuous manner

- It brings transparency in the budget formulation process

- It helps in decision making regarding allocation of funds

- It acts as a tool for reviewing efficiency of programs

- It integrates the process of planning, programming & budgeting

Limitations of Performance Budgeting

- It focuses on quantitative evaluation rather than qualitative evaluation.

- It is ineffective without a proper and systematic accounting and reporting system.

- It is difficult to quantify social benefits.

- It is difficult to accurate estimate benefits arising out of each activity.

Also Read: Zero-Based Budgeting

На дом выезжает квалифицированный врач, который проводит процедуру детоксикации в комфортных условиях, позволяя пациенту избежать стресса и огласки. С помощью капельницы и медикаментов нормализуется состояние, восстанавливаются основные функции организма. Процедура длится несколько часов, после чего врач оставляет рекомендации по поддерживающему лечению.

Получить дополнительные сведения – вывод из запоя цена

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Получить дополнительные сведения – vyvod iz zapoya kruglosutochno

Психологическая помощь не менее важна: наши специалисты проводят как индивидуальные, так и групповые сеансы, где вы учитесь справляться с тревогой, формировать новые навыки стресс-менеджмента и находить мотивацию к трезвому образу жизни. Диетолог составит персональный план питания, учитывающий потребности восстановленного организма, а мобильное приложение клиники позволит оставаться на связи с врачом 24/7 — вы всегда получите совет и поддержку.

Ознакомиться с деталями – https://kapelnica-ot-zapoya-moskva1.ru/kapelnica-ot-zapoya-cena-v-balashihe/

Вернуть здоровье и силы за одну процедуру позволяет грамотное сочетание препаратов, подобранное индивидуально под каждого пациента. Врач-нарколог оценивает тяжесть интоксикации, измеряет артериальное давление, пульс и уровень насыщения крови кислородом, а при необходимости назначает экспресс-анализы. На основании этих данных создаётся персональный раствор для инфузии:

Получить дополнительные сведения – https://kapelnica-ot-zapoya-moskva1.ru/kapelnicy-ot-zapoya-na-domu-v-balashihe

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Получить больше информации – vyvod iz zapoya anonimno

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Получить больше информации – https://vyvod-iz-zapoya-lyubertsy2.ru/vyvod-iz-zapoya-anonimno/

Запой — тяжёлое состояние алкогольной зависимости, при котором организм постоянно подвергается токсическому воздействию алкоголя. Это не просто неприятное явление, а угрожающее жизни состояние, которое требует немедленного медицинского вмешательства. Наркологическая клиника «Воздух Свободы» в Люберцах предлагает профессиональный и эффективный вывод из запоя с индивидуальным подходом и максимальным уровнем конфиденциальности.

Исследовать вопрос подробнее – http://vyvod-iz-zapoya-lyubertsy2.ru/vyvod-iz-zapoya-anonimno/

На дом выезжает квалифицированный врач, который проводит процедуру детоксикации в комфортных условиях, позволяя пациенту избежать стресса и огласки. С помощью капельницы и медикаментов нормализуется состояние, восстанавливаются основные функции организма. Процедура длится несколько часов, после чего врач оставляет рекомендации по поддерживающему лечению.

Изучить вопрос глубже – вывод из запоя на дому люберцы

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Изучить вопрос глубже – http://vyvod-iz-zapoya-lyubertsy2.ru

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Подробнее тут – vyvod iz zapoya anonimno

Родные не всегда сразу могут осознать серьёзность ситуации, однако существуют определённые симптомы, при появлении которых важно незамедлительно вызвать врача-нарколога:

Узнать больше – https://vyvod-iz-zapoya-lyubertsy2.ru/vyvod-iz-zapoya-anonimno

На дом выезжает квалифицированный врач, который проводит процедуру детоксикации в комфортных условиях, позволяя пациенту избежать стресса и огласки. С помощью капельницы и медикаментов нормализуется состояние, восстанавливаются основные функции организма. Процедура длится несколько часов, после чего врач оставляет рекомендации по поддерживающему лечению.

Получить больше информации – https://vyvod-iz-zapoya-lyubertsy2.ru/srochnyj-vyvod-iz-zapoya/

В клинике «Воздух Свободы» процедура вывода из запоя в Люберцах начинается с комплексной диагностики. Врач проводит первичный осмотр, измеряет жизненные показатели и подбирает препараты, которые быстро снимают симптомы интоксикации. В зависимости от состояния пациента, лечение может проходить дома или в стационаре клиники.

Исследовать вопрос подробнее – вывод из запоя круглосуточно

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Детальнее – вывод из запоя на дому

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Разобраться лучше – vyvod iz zapoya dzerzhinskij

В клинике «Воздух Свободы» процедура вывода из запоя в Люберцах начинается с комплексной диагностики. Врач проводит первичный осмотр, измеряет жизненные показатели и подбирает препараты, которые быстро снимают симптомы интоксикации. В зависимости от состояния пациента, лечение может проходить дома или в стационаре клиники.

Получить дополнительную информацию – https://vyvod-iz-zapoya-lyubertsy2.ru/vyvod-iz-zapoya-na-domu/

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Разобраться лучше – https://vyvod-iz-zapoya-lyubertsy2.ru/

По словам врача-нарколога клиники «Воздух Свободы» Дмитрия Соколова: «Чем раньше начнётся профессиональная терапия, тем меньше шансов, что последствия запоя будут серьёзными и необратимыми».

Углубиться в тему – вывод из запоя цена

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Подробнее тут – vyvod iz zapoya nedorogo

Домашний формат идеально подходит для тех, кто находится в удовлетворительном состоянии и не требует круглосуточного контроля.

Исследовать вопрос подробнее – vyvod iz zapoya lyubercy

По словам врача-нарколога клиники «Воздух Свободы» Дмитрия Соколова: «Чем раньше начнётся профессиональная терапия, тем меньше шансов, что последствия запоя будут серьёзными и необратимыми».

Исследовать вопрос подробнее – vyvod iz zapoya kapelnica

В клинике «Воздух Свободы» процедура вывода из запоя в Люберцах начинается с комплексной диагностики. Врач проводит первичный осмотр, измеряет жизненные показатели и подбирает препараты, которые быстро снимают симптомы интоксикации. В зависимости от состояния пациента, лечение может проходить дома или в стационаре клиники.

Выяснить больше – https://vyvod-iz-zapoya-lyubertsy2.ru/

По словам врача-нарколога клиники «Воздух Свободы» Дмитрия Соколова: «Чем раньше начнётся профессиональная терапия, тем меньше шансов, что последствия запоя будут серьёзными и необратимыми».

Подробнее можно узнать тут – http://vyvod-iz-zapoya-lyubertsy2.ru

В клинике «Воздух Свободы» процедура вывода из запоя в Люберцах начинается с комплексной диагностики. Врач проводит первичный осмотр, измеряет жизненные показатели и подбирает препараты, которые быстро снимают симптомы интоксикации. В зависимости от состояния пациента, лечение может проходить дома или в стационаре клиники.

Изучить вопрос глубже – https://vyvod-iz-zapoya-lyubertsy2.ru/

На дом выезжает квалифицированный врач, который проводит процедуру детоксикации в комфортных условиях, позволяя пациенту избежать стресса и огласки. С помощью капельницы и медикаментов нормализуется состояние, восстанавливаются основные функции организма. Процедура длится несколько часов, после чего врач оставляет рекомендации по поддерживающему лечению.

Исследовать вопрос подробнее – https://vyvod-iz-zapoya-lyubertsy2.ru/vyvod-iz-zapoya-anonimno/

Запой — одно из самых опасных проявлений алкогольной зависимости. Он сопровождается глубокой интоксикацией организма, нарушением работы сердца, печени, головного мозга и других жизненно важных систем. Когда человек не может остановиться самостоятельно, а организм больше не справляется с нагрузкой, требуется медицинская помощь. В наркологической клинике «Спасение» в Мытищах мы проводим экстренные процедуры инфузионной терапии, позволяющие эффективно и безопасно вывести пациента из состояния запоя. Капельница — это первый шаг на пути к восстановлению здоровья и возвращению к нормальной жизни.

Подробнее тут – https://kapelnica-ot-zapoya-moskva2.ru/

Многие недооценивают последствия запоя, особенно если речь идёт о человеке, который ранее не испытывал серьёзных проблем со здоровьем. Однако даже несколько дней непрерывного употребления алкоголя способны вызвать тяжёлые системные сбои. Нарушается кислотно-щелочной и водно-солевой баланс, кровь становится густой, затрудняется работа сердца. Печень перестаёт эффективно обезвреживать токсины, и продукты распада этанола поступают в мозг, вызывая когнитивные и поведенческие нарушения.

Выяснить больше – http://kapelnica-ot-zapoya-moskva2.ru/